NEWS Release - Speech by Governor Jerome H. Powell - At the Forecasters Club of New York Luncheon, New York, New York - February 22, 2017

The Economic Outlook and Monetary Policy

Thank you for this invitation to speak here today. I will begin by taking stock of the progress of the U.S. economy. I will then discuss longer-term challenges for the economy and wrap up with a discussion of monetary policy. As usual, my comments reflect my own views and not necessarily those of my colleagues on the Federal Open Market Committee (FOMC).

The Current State of the Economy

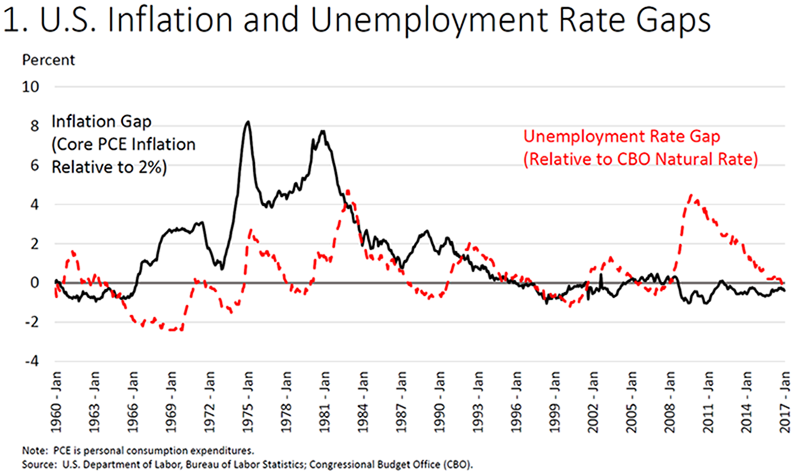

The Congress has tasked the Federal Reserve with achieving stable prices and maximum employment--the dual mandate. The FOMC has set a longer-term price stability objective of 2 percent annual inflation, as measured by the PCE (personal consumption expenditures) price index.1 This is a symmetric objective, meaning that the Committee would be concerned if inflation were running persistently above or below 2 percent. Until early last year, inflation was running substantially below our 2 percent objective, largely reflecting declines in energy prices during late 2014 and early 2015. However, because prices of energy and food commodities are often volatile, a core measure that excludes these components provides a better indication of where overall inflation is headed. While core inflation has also run consistently below 2 percent in recent years, it has been gradually rising, with the most recent 12-month reading at 1.7 percent, three-tenths higher than a year ago (the black line in figure 1). Market-based measures of inflation compensation have moved well above their lows of mid-2016 but remain below pre-crisis levels, and survey measures have stayed relatively well anchored. Overall, inflation seems to be on track to reach the 2 percent objective over the next couple of years. Although inflation is currently below our objective, core inflation has generally been close to 2 percent over the past 20 years. This outcome reflects the success of monetary policy in anchoring inflation expectations.

{kind=link}

Many indicators show that we have also made significant progress toward maximum employment. Since 2010, payroll employment has increased by almost 16 million jobs, and the unemployment rate has fallen from 10 percent to 4.8 percent--in line with most estimates of the longer-run normal level (or natural rate) of unemployment and with the median estimate by FOMC participants in the December 2016 Summary of Economic Projections (SEP). Accordingly, the red line in the figure indicates that the unemployment rate gap has essentially been closed.2

A variety of other measures also suggest that we are close to maximum employment. Surveys of household sentiment about the availability of jobs and of business sentiment regarding the difficulty of filling jobs have now reached levels seen in prior periods of full employment. Moreover, although the pace of wage increases is slower than during pre-crisis periods of full employment, wages have been increasing faster than both output per hour (productivity) and inflation, and labor's share of income has begun to move up after a long decline.

All in all, we appear to be close to our employment objective, and are nearing our inflation objective. While the pace of progress has at times been frustratingly slow, this outcome is a better one than that achieved by most other advanced economies. Even so, it is worth remembering that the current and future states of the economy are always uncertain, and today is no exception. Our discussions of the economy may sometimes ring in the ears of the public with more certainty than is appropriate. Take the concept of "maximum employment," which requires an estimate of both the natural rate of unemployment for those who are in the labor force and the sustainable level of labor force participation.3The natural rate of unemployment is not directly observed, and the record suggests that it could be materially lower or higher than current estimates.4 There is also uncertainty about the underlying trend level of labor force participation.

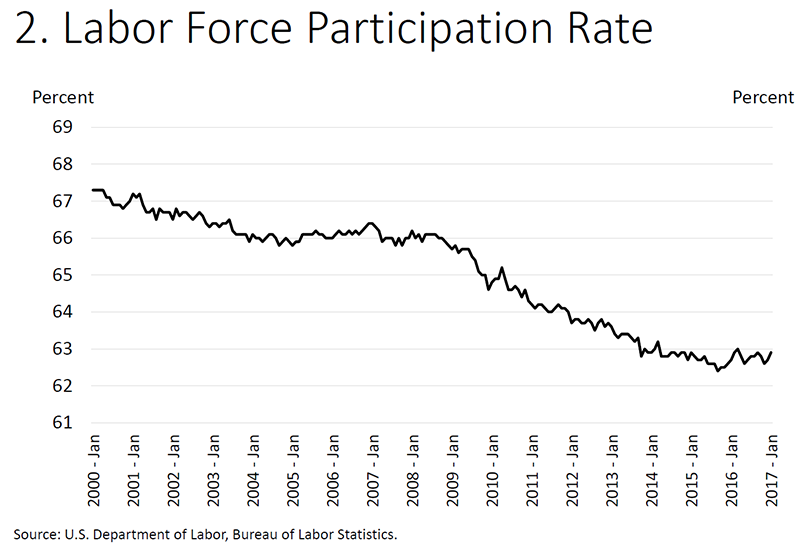

Participation has been declining since about 2000 because of the aging of our population and other secular trends, and analysts generally agree that participation will continue to decline over time for these reasons (figure 2). A canonical paper by a group of Fed economists estimates a trend rate of decline of about 0.3 percentage point per year.5 After declining sharply and dipping well below the prior trend in the years following the crisis, participation has been roughly flat since late 2013. Relative to this estimate of the declining trend, three years of flat participation implies a cyclical improvement of roughly 1 percentage point. But there is a range of views on the underlying trend and whether we can expect a bit more near-term cyclical improvement in participation. The Congressional Budget Office estimates that participation is currently 0.7 percentage point below its trend rate, which suggests remaining upside potential. By contrast, other recent work does not find a strong case for a meaningful further slack.6 The issue has important implications, since changes in participation can have material effects on the unemployment rate: Holding the level of employment constant, a 25 basis point change in the participation rate would lead roughly to a corresponding 40 basis point change in the unemployment rate.

{kind=link}

20th Street and Constitution Avenue N.W.

Washington, D.C. 20551

page source https://www.federalreserve.gov/